What to Know About Fringe Benefits Tax in 2026

The 2025/2026 Fringe Benefits Tax (FBT) year ends on 31 March 2026. Here’s what you need to know.

What is FBT?

Fringe Benefits Tax is payable by employers on the value of certain benefits provided to employees or their associates in respect of their employment. FBT applies to a range of benefits provided to employees and deemed employees (which includes, but is not limited to, spouses of employees).

Examples of Fringe Benefits

- An employer’s ‘car’ that is used or available for an employee’s (or director’s) private use

- Car parking

- Loans to employees

- Housing/accommodation for personal use

- Non business travel

- Paying private expenses e.g. holidays, health insurance and gym memberships

- Advances of money e.g. short term loan

- Providing food, drinks and other entertainment expenses (includes business lunches and Christmas parties)

- Giving gifts – whether it be from stock on hand or other items like gift cards

Exemptions and reductions of Fringe Benefits

There are many exemptions for benefits provided that either have a nexus with work related items or a value of less than $300 and are infrequent/irregular in nature. Employers may not always be subject to FBT, but it’s important to review expenditure each year to ensure obligations are met.

Generally, any employee contributions towards the cost of providing a fringe benefit (e.g. fuel paid for a car) will reduce the taxable value of the fringe benefit. Certain electric vehicles (but not PHEVs) may be exempt from FBT, although are still reportable fringe benefits for employees, so records must still be kept for calculations.

Company Vehicles For Personal Use

A common benefit many clients provide is private use of company vehicles by business directors/owners. Whilst it is appealing to purchase personal vehicles in the business to claim depreciation and running expenses, there is an additional cost to be mindful of.

The liability on a company car driven by a director/owner of a business can however be negated by employee contributions or loan funds advanced rather than the company paying tax at 47%.For personal use of cars, whether by directors/associates or employees, there are two available calculation methods:

- Statutory Method

- Operating Cost Method

Statutory Method:

This method uses a flat, statutory rate to calculate the taxable value. The current rate is 20% of the original cost of the vehicle (including GST but excluding stamp duty). After 4 full FBT years, a ‘reduced cost’ method may be used which is 2/3 of the original cost. The Statuary Method is a very simple calculation, although for vehicles with low private use, may not result in the most favourable outcome.

Operating Cost Method (Log Book Method):

This method is calculated by adding together all of the running costs (fuel, registration, insurance and repairs & maintenance, inclusive of GST), interest (at the ATO’s determined rate) and depreciation, then multiplying by the percentage of private use, determined by a valid log book.

Motor vehicle odometer readings should be recorded on 31 March each year. The log book method is great if private use is relatively low, but requires more diligent record keeping in maintaining the log book and running expenses.

The result of either method is the taxable value which is then multiplied by a gross up factor and the tax rate of 47%. Where the information is available, it is best to calculate both methods to ascertain the most favourable outcome.

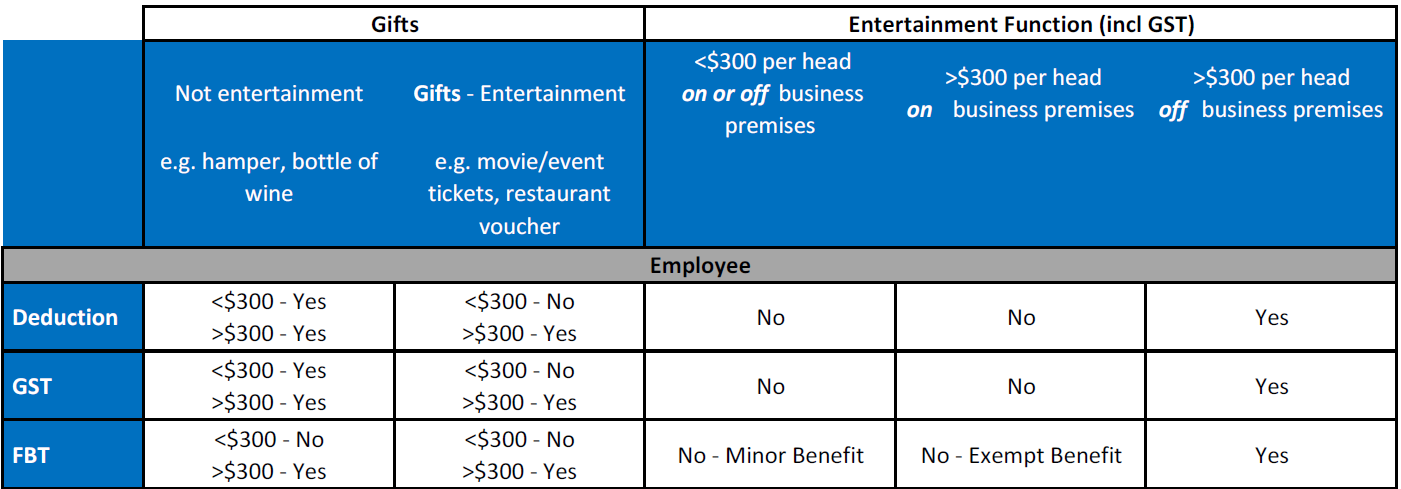

Gifts & Entertainment

Navigating FBT application, expense deductibility for income tax and GST claims can be a minefield. Associates and clients must also be considered as there are different treatments depending on who is receiving the benefit. A summary of gift and entertainment benefits that may be provided to an employee is shown below.

If navigating Fringe Benefits Tax is something you need support with, get in touch.

Photo by Erik Mclean on Unsplash

News & Insights

.jpg)

Important Changes from 1 July: New Client Verification Requirements

From 1 July, businesses providing certain designated professional services, including accounting firms, will be required to comply with Australia’s Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) legislation.

What the Payday Super Changes Mean for Employers

Australia’s superannuation system is about to undergo a major change. From 1 July 2026, employers will need to pay superannuation at the same time as wages, rather than quarterly.

Division 296: Superannuation Legislation Update

It was hard to escape the media coverage of Labor’s proposed superannuation tax legislation changes earlier this year, impacting those with superannuation balances above $3 million. Since the initial announcement garnered criticisms from many, we’ve received some welcome revisions from the Federal Government. Read on to learn what the tax is, the changes that’ve been made and who it will affect.

Division 7A: What Every Private Company Owner Needs to Know

Division 7A is legislation designed to prevent private companies from distributing profits to shareholders or their associates in the form of loans, payments, or debt forgiveness instead of taxable dividends or wages. A common example of this is for a business owner to transfer money to themselves over and above their wage or for the business owner to pay for something on the company credit card that is not deductible. Whilst the rules are relatively complex, here is a summary of what you need to know.